Planning Ahead: Social Security

Originally published on LinkedIn May 27, 2024

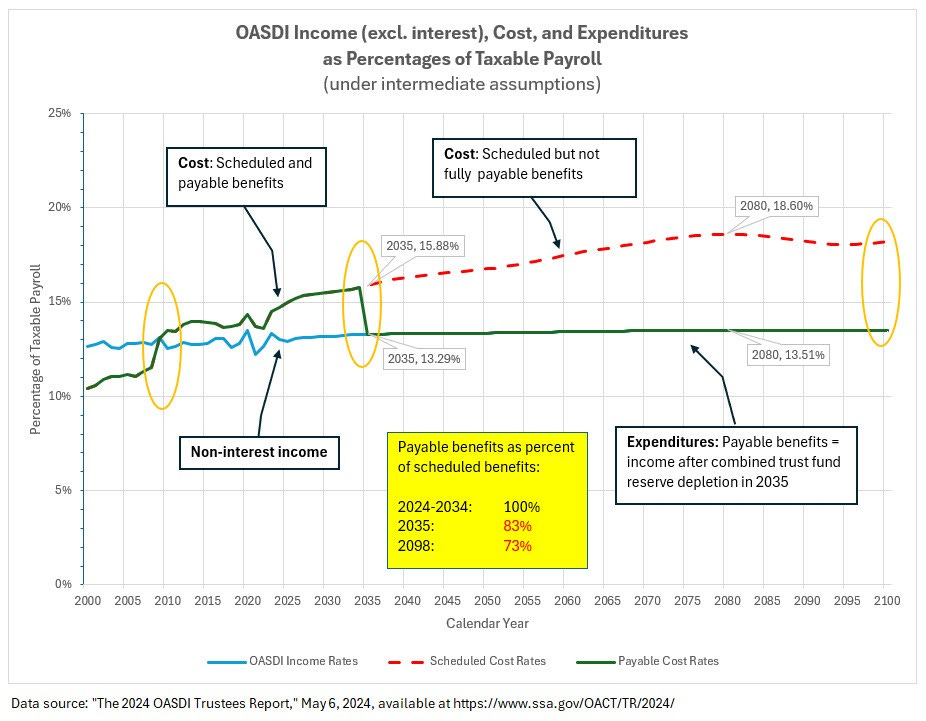

![OASDI Income, Cost, and Expenditures as Percentages of Taxable Payroll [Under intermediate assumptions]](https://substackcdn.com/image/fetch/$s_!uYpC!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F101ef9ab-353c-4b45-ac9d-fea909000a51_924x720.jpeg "OASDI Income, Cost, and Expenditures as Percentages of Taxable Payroll [Under intermediate assumptions]")

This has been another busy month of learning across several areas I've written about before, but the most significant topic that I achieved greater understanding in is related to Social Security in the context of Retirement Planning, which was my focus this term at Stetson University College of Law.

Most people in the US have probably heard Social Security is not quite as secure as it used to be, but many people would be hard pressed to explain exactly why and what could be done to shore it up for future generations. The sirens have been ringing for years already since 2010 when expenditures started exceeding payroll taxes, the primary source of funding, for the first time. Since then, projections have varied as far as how much longer the current benefits could be sustained before changes would be needed to address the income shortfall.

What's the problem exactly?

Earlier this month, the trustees for the 2 main funds involved in providing Social Security benefits (Disability being maintained separately from Old Age and Survivors, although they are frequently combined together for reporting purposes as OASDI), provided their latest reports and projections showing the reserve funds being tapped out by 2035 if nothing else is done to adjust income or benefits (or both!) to balance the program. Figure II.D2.—OASDI Income, Cost, and Expenditures as Percentages of Taxable Payroll [Under intermediate assumptions] is available in the report, but I found it easier to interpret with color and additional callouts as shown below.

What makes this chart so helpful in putting things in perspective is just how much of a gap there is between the planned benefits and expenditures starting in 2035 - this is when the reserves may run out that have been covering the gap since 2010. At that point, if no adjustments in taxes are made, benefits may be cut by around 17%. The gap will continue to widen to its maximum point in 2080 before closing a bit by 2098, the end of the 75-year projection period. Either way, recipients are looking at up to a 27-28% cut in benefits if no other changes are made to address the projected shortfall.

I should note as in the report highlights that this is where it is helpful to keep in mind that the Disability Fund is actually forecast to remain sound during this period, and it is the much larger OAS share of the funds that is seeing this gap starting in 2033. By combing them, it appears they may have more time to 2035.

Considered separately, the reserves of the OASI Trust Fund are projected to become depleted during 2033 under the intermediate assumptions. The reserves of the DI Trust Fund along with projected program income are sufficient to cover projected program cost over the next 10 years. The OASI Trust Fund fails the test of short-range financial adequacy, but the DI Trust Fund satisfies the test.

Either way, it is clear something needs to change if many people are still relying on Social Security as a significant part of their retirement planning. Given concerns about ongoing inflation impacts, as well, the cliff may be even more significant when reserves run out.

How do we fix it?

There are a number of proposals that have been circulating for years to address various aspects of the program. Many of them have been categorized for analysis by the Office of the Chief Actuary based on the following:

A summary of the impact of these changes is also available for reference, but one quick glance will tell you this is not a simple exercise to find the right combination that would be feasible in the current climate.

A great tool that can help distill the major options is available from the American Academy of Actuaries called the Social Security Challenge. It's very informative for people unfamiliar with the current programs and challenges and gives everyone a chance to try their hand at choosing the right combination of changes to eliminate the shortfall.

I'm not going to tell you which options I chose, but I am happy with the options I selected and now I can better advocate for them where I can! I hope you will be able to do the same now, too.

Reference

American Academy of Actuaries, "Social Security Challenge," at https://www.actuary.org/socialsecurity

Johnston, David Cay, "What's Going on with Social Security — and How Concerned Should You Be?," Kiplinger, Mar. 25, 2024, at https://www.kiplinger.com/retirement/social-security/the-looming-crisis-for-social-security

National Academy of Elder Law Attorneys (NAELA)

https://www.naela.org/

Social Security Administration (SSA)

https://www.ssa.gov/SSA, "2024 OASDI Trustees Report" https://www.ssa.gov/OACT/TR/2024/trTOC.html

SSA, "Office of the Chief Actuary's Estimates of Proposals to Change the Social Security Program or the SSI Program," at https://www.ssa.gov/OACT/solvency/index.html

SSA, "Summary of Provisions That Would Change the Social Security Program," at https://www.ssa.gov/OACT/solvency/provisions/cola_summary.html

Stetson University College of Law Center for Elder Justice https://www.stetson.edu/law/academics/elder/home/

U.S. Bureau of Labor Statistics, Consumer Price Index https://www.bls.gov/cpi/home.htm